A Compelling Solution for Investors When Debt Replacement Requirements Take Precedence

On the surface, the premise does not make much sense. Why would an investment property owner conducting a 1031 exchange, invest in a replacement property designed to generate no income? After all, isn’t that the general intent of investment property ownership – to enjoy a consistent stream of income from monthly rent payments and even perhaps benefit from the property’s appreciated property value upon a sale?

While most would agree this a primary appeal of real estate investing, there are situations where investors may have other objectives. For example, when meeting the debt replacement requirement of a 1031 exchange is a concern in order to avoid tax implications, an investment in a property that accommodates a high amount of debt placement, may actually be appealing. Highly leveraged, zero cash flow properties may be an attractive option for these types of situations.

What are Zero Cash Flow Properties?

Zero cash flow properties (zeros) are traditionally triple net leased (NNN) commercial real estate assets with well-established, creditworthy tenants that hold investment-grade ratings. Zeros are highly leveraged – loan-to-value (LTV) at 80 to 90 percent – with long-term lease agreements. As a result, all net operating income (NOI) generated by the property is used to pay the debt service obligation on the mortgage loan, and therefore provides no cash flow to the investor.

Zeros are available in a variety of asset types including corporate office buildings, grocery, retail, and industrial. They are most commonly desired by 1031 exchangers who have high debt replacement requirements.

How a Zero Works

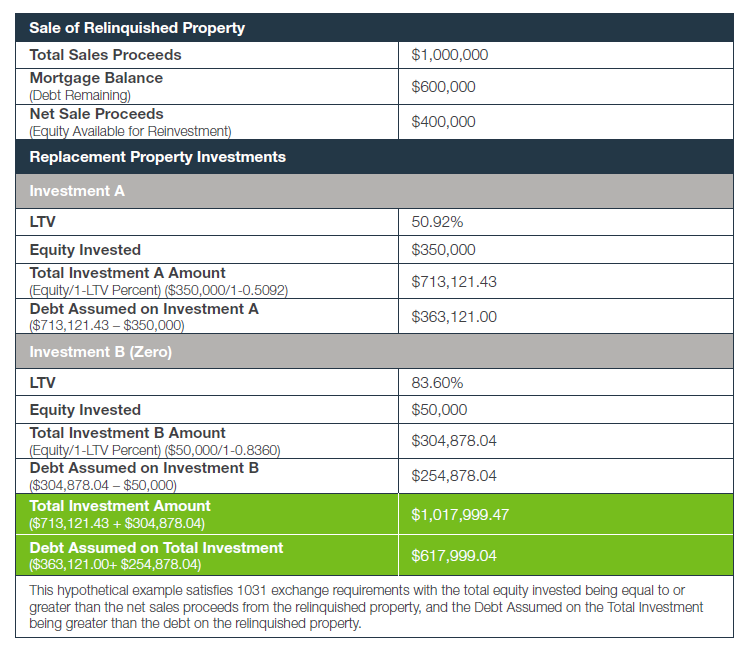

This example helps illustrate how a typical investor might use a zero.

An investor is coming out of a moderately leveraged property sale with $400,000 equity left for reinvestment. To fulfill the debt requirement of the 1031 exchange and avoid tax implications, the sum of the cash invested and the debt placed on the replacement property must be equal to or greater than the sum of the cash invested and debt placed on the relinquished property.

The investor chooses two replacement property investments, one with an average LTV and the second is a zero cash flow investment with a high LTV. Here is how a zero would be utilized to meet this investor’s needs.

Other Advantages of Zeros

Zeros offer investors other advantages including:

- Potential taxable net losses: Ability to offset taxable income generated elsewhere in a portfolio

- In-place loan acquisition: Investors are not restricted by lack of financing options

- Consistent market need: Many 1031 exchanges require both an equity and debt requirement that a zero may help fulfill

Who Are Zeros Appropriate For?

As mentioned, investors who are primarily concerned about satisfying the debt replacement requirement of a 1031 exchange are those who would have greatest interest in zeros. These investors might have little or no equity left from the sale of a relinquished property and may utilize a zero to acquire real estate with as little equity as possible.

In addition, zeros may have appeal to non-exchange buyers who want to invest in institutional grade real estate that may produce net tax losses which could offset income in other areas of their portfolios.

We hope this information has been helpful in highlighting this lesser known but important investment option for real estate investors. If you have any additional questions, do not hesitate to reach out to your wholesaler today!

This is not intended as tax advice. Prospective investors should consult with their own tax advisor regarding an investment in an IPC-sponsored program.