Adopting an Alternative CRE Strategy to Meet Today’s Market Challenges

Investors will remember 2022 as a year when markets delivered a one-two punch that shattered investments and upended long-held beliefs about portfolio construction. The S&P 500 finished the year down 19.4 percent, making it one of the worst years on record since the Great Depression. And the Bloomberg U.S. Aggregate bond index ended down 12 percent, its worst year in the history of the index.1

The revered 60/40 stock and bond portfolio not only failed to protect investors, but it also forfeited all the extraordinary gains from the previous two years. With investor confidence shaken, advisors now face a variety of challenges that will likely require them to explore and adopt investments beyond stocks and bonds and ask important questions about which solutions will be most suitable for their clients.

In essence, we believe 2022 was a pivotal year that will begin to usher in the wide use of alternative investments in portfolio construction to provide the diversification, returns, and portfolio stability clients are looking for. Welcome to the Great Reallocation.

Addressing Today’s Unique Challenges

Inflation

Inflation, dormant for decades, rose to its highest level in 40 years in June 2022.2 Inflation reduces the purchasing power of money and erodes the value of many assets.

Pandemic stimulus by central banks, consumer demand, global supply shortages, international conflict, and deglobalization contributed to setting inflationary forces in motion.

Some hoped inflation would be transitory. However, inflation has persisted well into 2023 despite the tough economic medicine given by policymakers.

Rising Rates

Interest rates – once low, near zero, and even negative in some markets –have risen significantly following seven rate increases by the Federal Reserve (the Fed) in 2022.3 And more increases have continued in 2023. As a result, economic activity has begun to slow in certain sectors due to the rising cost of capital. Higher rates typically have a negative impact on asset values.

Fed Easing to Fed Tightening

The Fed directed global economic rescues after the Great Financial Crisis of 2007 to 2009 and the 2020 COVID-19 pandemic. Fed easing included near-zero short-term interest rates. Fed stimulus also included massive bond buying to drive down long-term rates and provide cash for the financial markets and broad economy. As a result, the Fed’s balance sheet swelled from just under $1 trillion in March 2008 to nearly $9 trillion by March 2022.4

The Fed is now normalizing after years of extraordinary policies, moving from easing to tightening, raising benchmark interest rates, and allowing its balance sheet to shrink. By normal markets, we mean more volatility, which will require risk management, careful investment selection, and a nimble approach to opportunity.

Economic Slowdown

Recent bank failures have exacerbated recession concerns, compounding the impact of rising rates, higher inflation, and tightening financial conditions. Some economic sectors appear resilient, others vulnerable.

Return of Volatility

After years of low volatility in financial markets, stocks and bonds have exhibited gyrations not seen in years.

In light of these serious headwinds, investors and financial professionals must rethink investment strategies and the way portfolios are constructed. The need for resilient assets is paramount.

The Great Reallocation

The move to an alternative allocation model has begun, with the allocation to alternative investments increasing to meet the investment challenges of our changing times. Portfolio allocation now requires a multidimensional approach. Resilient portfolios now include stocks, bonds, and alternative investment strategies.

Institutional investors understand the power of adding alternatives to a diversified portfolio. The 60/40 model of yesteryear is giving way to a more diversified allocation of 50/30/20 or even a 40/30/30 allocation across stocks, bonds, and alternatives.

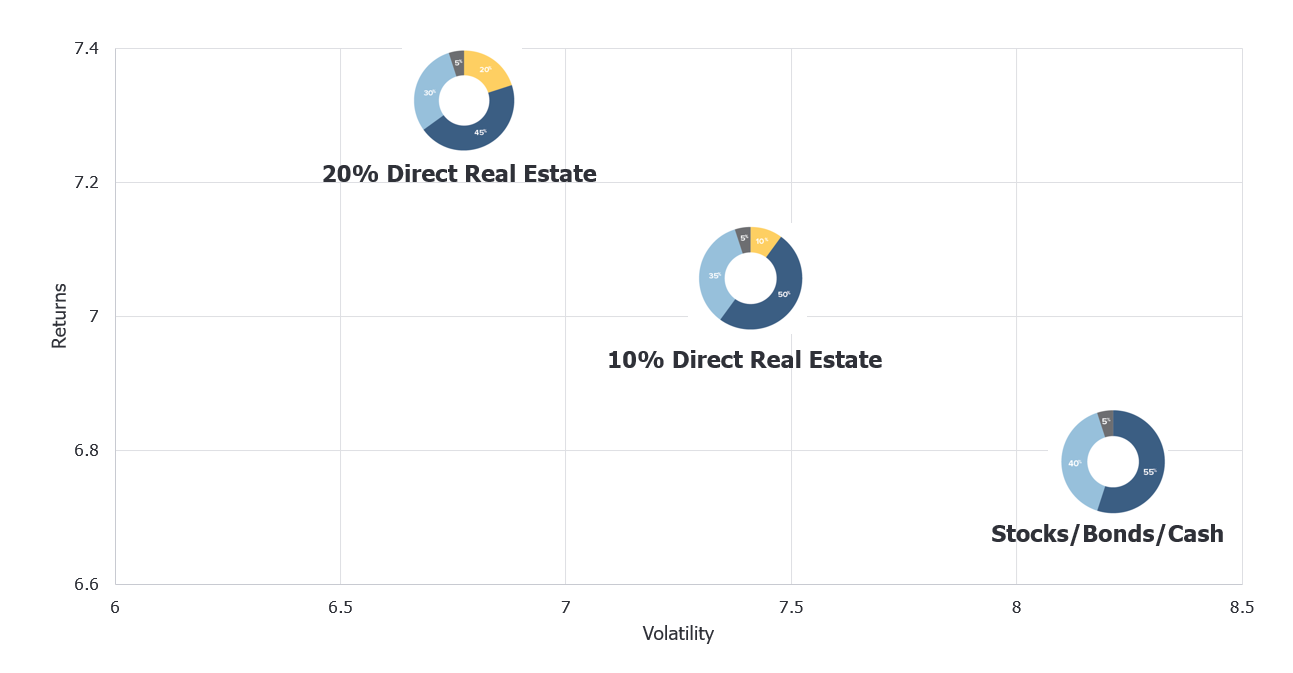

For example, a 20 percent allocation to real estate can improve the long-term risk/return profile of a diversified portfolio.

Improving Diversification and Risk/Return Profiles with Real Estate*

According to the recent CAIS/Mercer survey, nearly 90 percent of advisors intend to increase alternative assets (alts) allocations in the next two years, many targeting 15 to 25 percent or more of their client portfolios for alts.5

CAIS/Mercer Survey: Advisors Increasing Target Allocations to Alternatives

2023-2024

|

Alts Allocation Target |

15%+ |

25%+ |

|

% of Advisors |

53% |

21% |

Source: WealthManagement.com

Innovative Alternative Solutions

In our era of innovation, financial professionals and investors alike have access to a growing range of alternative investments. Specialized alternative investment solutions include commercial real estate, some sectors with a long history of resilience in the face of inflation and economic uncertainty.

In upcoming blogs, we will discuss which alternative commercial real estate sectors we believe are well-positioned to withstand, and possibly outperform in the current economic environment.

---

*Past performance is not a guarantee of future results. Charts for illustrative purposes only. An investment in ALT REIT is not a direct investment in real estate and has material differences from a direct investment in real estate, including those related to fees and expenses, liquidity and tax treatment. Investing 10 or 20 percent in direct real estate both increased the portfolio’s total return and lowered the portfolio’s overall standard deviation. The charts above compare the returns of the S&P 500 Index, Barclays U.S. Aggregate Bond Index and the NCREIF (National Council of Real Estate Investment Fiduciaries) Index, with and without an asset allocation to direct real estate, over a 20-year time period. Standard deviation is a measurement of the variability of an investment, derived from its historical returns. A higher standard deviation indicates a greater variability of an investment. The S&P 500 Index is a market capitalization weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance. The Barclays U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. The Index includes Treasuries, government-related and corporate securities, mortgage backed securities, adjustable rate mortgage pass-through asset backed securities, and commercial mortgage backed securities. NCREIF Property Index (NPI) is the accepted index created to provide an instrument to gauge the investment performance of the commercial real estate market. NPI is an index that reflects the returns of a large pool of individual commercial real estate properties, is leverage free with no fees and includes a blended pool of institutional quality properties. Each index provides a broad representation of a particular asset class and is not indicative of any investment. Asset allocation does not ensure a profit or protect against a loss. The rates of returns shown do not reflect the deduction of fees and expenses inherent in investing. An investment cannot be made directly in an index. ALT REIT has material differences from a direct investment in real estate, including related to fees and expenses, liquidity and tax treatment.

2 bls.gov