Have Clients with Crypto Gains?

Help them defer their capital gains and access impact investing

with Qualified Opportunity Zones

As an advisor, you may know investors with large, taxable cryptocurrency gains who may need your help investing those taxable gains to potentially become eligible for favorable tax treatment. Many may also be interested in investment opportunities with a positive social impact. Enter Qualified Opportunity Zones (QOZs), which unite tax-advantaged and impact investing.

Cryptocurrency investments are known to be extremely volatile, and not all investors have found crypto success. Yet many crypto traders have accumulated wealth they would like to protect. QOZs may help meet that objective.

Reducing Tax Liability on Cryptocurrency Gains

When the Opportunity Zone Program was created under the 2017 Tax Cuts and Jobs Act, the program was intended to stimulate private investment in more than 8,700 designated economically distressed communities throughout the U.S.

The QOZ program's tax incentives are significant and may appeal to a wide range of investors. Unlike 1031 exchanges which enable investors to defer capital gains taxes when selling real estate investment property, QOZ investments allow investors to defer capital gains tax on the sale of a wider variety of asset types.

By investing in a QOZ, an investor can defer capital gains tax on the sale of stocks, mutual funds, bonds, real estate, business, jewelry, art, collectibles, and cryptocurrencies. This tax benefit, along with the intended goal of revitalizing underserved communities, considerably expands the investor pool interested in QOZ opportunities.

The Prototypical Investor?

QOZ programs are generally only available to accredited investors, commonly defined as:

"Anyone who earned income that exceeded $200,000 (or $300,000 together with a spouse or spousal equivalent) in each of the prior two years, and reasonably expects the same for the current year, or, has a net worth over $1 million, either alone or together with a spouse [or spousal equivalent]." - investor.gov

Most accredited investors in the U.S. are 50 years or older1, so many sponsors have been surprised at the growing interest in QOZ investments among those 40 years and under.2 A good portion of these new tax-savvy investors could be cryptocurrency traders who have amassed wealth in a relatively short period.

Does Crypto Qualify?

In the early days of cryptocurrency, there were questions about if and how crypto transactions should be taxed. But in 2014, the IRS definitively answered those questions as highlighted in the CPA Journal, January, 2019: by stating:

"Taxpayers must recognize gain or loss on the exchange of cryptocurrency for cash or for other property. Accordingly, gain or loss is recognized every time that cryptocurrency is sold or used to purchase goods or services."

The IRS defined “virtual currencies” as property for tax purposes since they are not issued by a government or central bank. And as mentioned, QOZs allow investors to defer capital gains on any type of property, including cryptocurrencies.

Tax Incentives

An individual who invests in a qualified opportunity fund, which is the type of fund that owns a QOZ property (a QOF), is eligible for favorable tax treatment in the form of both tax deferral and forgiveness.

Tax Deferral

By investing capital gains in a QOF within 180 days of the gain's realization, an investor can defer taxation on the gain until December 31, 2026, or when the investor liquidates the QOF investment – whichever comes first.

Tax Forgiveness

By remaining invested in a QOF for ten years are longer, any gains on the investment are not subject to capital gains tax.

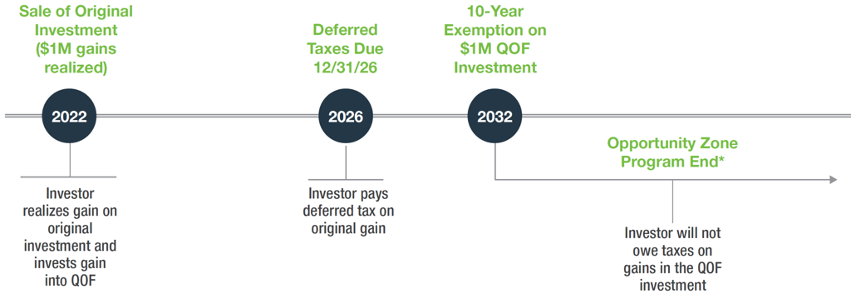

QOZ Investing Hypothetical Timeline

https://www.nar.realtor/infographics/qualified-opportunity-zone-investors-timeline. A QOF investment ends per terms outlined in the specific fund. If an investor holds an interest in a QOF for at least ten years, then, in connection with the sale of such interest, the investor's basis in such interest will be equal to the fair market value of such interest on the date it is sold if a specified tax election is made, thereby eliminating any federal income tax with respect to any appreciation in the value of the interest.

https://www.nar.realtor/infographics/qualified-opportunity-zone-investors-timeline. A QOF investment ends per terms outlined in the specific fund. If an investor holds an interest in a QOF for at least ten years, then, in connection with the sale of such interest, the investor's basis in such interest will be equal to the fair market value of such interest on the date it is sold if a specified tax election is made, thereby eliminating any federal income tax with respect to any appreciation in the value of the interest.

Two Bitcoin Investors. Two Different Outcomes.

To illustrate the potential tax benefits of a QOZ investment, let's look at two crypto investors -- one who invested crypto gains in a QOF and one who did not.

Steve and Gary each bought 1,000 bitcoin in 2013 at $100 per coin. Unlike many crypto investors who trade with high frequency, Steve and Gary held onto their bitcoin for several years, selling their positions throughout 2021 for an average price of approximately $40,000 per coin. They chose different paths with their profits.

|

Date |

Pays Taxes on Crypto Profits |

Reinvests Crypto Profits in QOF |

|

2013 |

Steve invests $10,000 in Bitcoin (100 Bitcoin at approx. $100/coin) |

Gary invests $10,000 in Bitcoin (100Bitcoin at approx. $100/coin) |

|

2021 |

Steve sells his Bitcoin for $4 million (100 Bitcoin at approx. $40,000/coin) |

Gary sells his Bitcoin for $4 million (100 Bitcoin at approx. $40,000/coin) |

|

March 2022 |

Steve reinvests his profits in a diversified portfolio. |

Gary chooses to defer his capital gains by investing in a QOF.

(Gary sets aside $1.2 million in a non-interest-bearing account as a reserve to pay his deferred capital gains that he has to recognize by Dec. 31, 2026 as the QOZ program requires.) |

|

April 2022 |

Steve files his 2021 Federal and State tax returns and pays approx. $1.2 million in tax on the appreciated gains of his Bitcoin sale. ($4 million in gains x 20% long-term capital gains tax + 3.8% net investment income tax + 5% state capital gains tax) |

Gary files his 2021 Federal and State tax returns and pays no tax on the appreciated gains of his Bitcoin sale. *

|

|

December 2026 |

Steve has already paid tax on his Bitcoin gains. |

|

|

April 15, 2027 |

|

Gary recognizes his gain by the 12/31/26 deadline and pays approx. $1.2 million in deferred tax on that gain when he files his 2027 Federal return. |

|

December 2032 |

Steve’s reinvested proceeds of $2.8 million have now grown in value to $5.6 million. He owes the IRS an additional $560,000 in capital gains tax. |

Gary’s reinvested proceeds of $2.8 million have also grown to $5.6 million. But his gains are eliminated from taxation because he held his QOF investment for 10 years. |

|

Total Tax Paid |

$1.76 million |

$1.2 million |

|

Total Value |

$4.56 million |

$5.6 million |

|

Additional After-Tax Gain |

$0 |

$1.04 million |

*Note that not all states allow QOZ tax breaks.

Obviously, not every cryptocurrency investor will experience the same types of gains illustrated in this example. But whether investors seek to defer long-term gains of $500,000 or $5 million, a QOZ investment offers a timely opportunity to help successful crypto investors capitalize on this unique tax benefit.